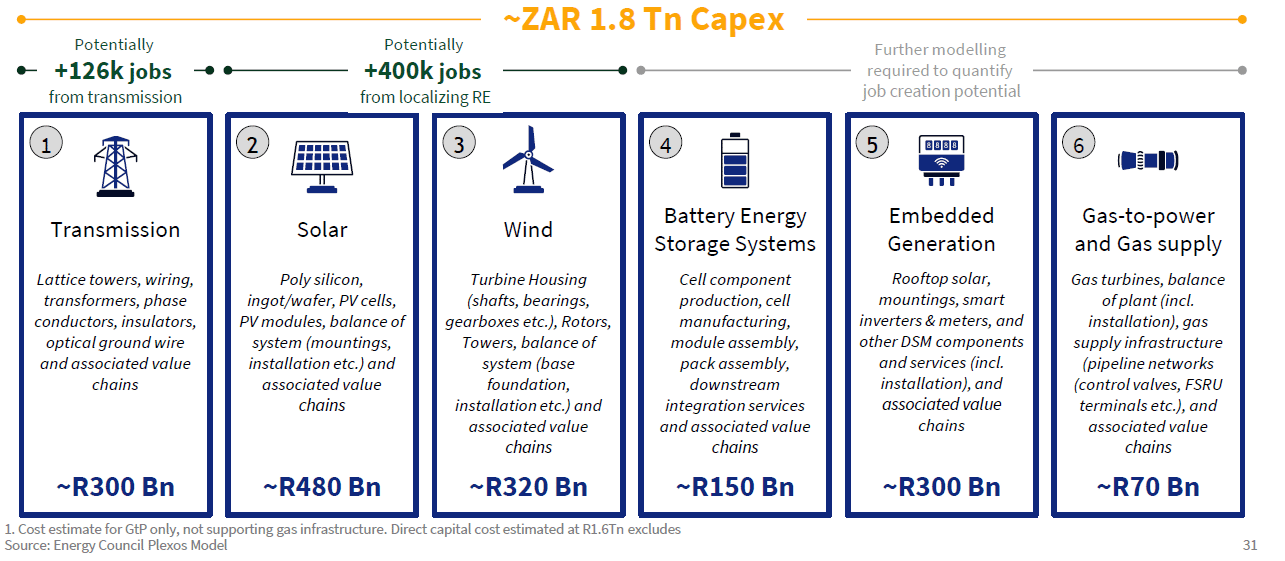

If we manage our energy transition properly, South Africa could unlock the largest ever capital investment programme in our history: R1.8-trillion over the next 10 years. This can be leveraged to rejuvenate local manufacturing, create meaningful jobs, and stimulate innovation and skills development for young people, and will ultimately #energisemzansi.

But “managing our affairs correctly” means dealing with two key issues:

Market reform is needed in South Africa both to ensure a competitive electricity sector for the benefit of customers, and to attract private sector investment for new generation and transmission.

No! Some of the groundwork has already been done. The recent signing into law of the Electricity Regulation Amendment Act (ERA) is a leap forward in reforming the market, because it makes provision for a multi-market power system with much more flexibility. This is significantly more attractive for businesses wanting to invest in energy projects, while also resulting in a better deal for consumers.

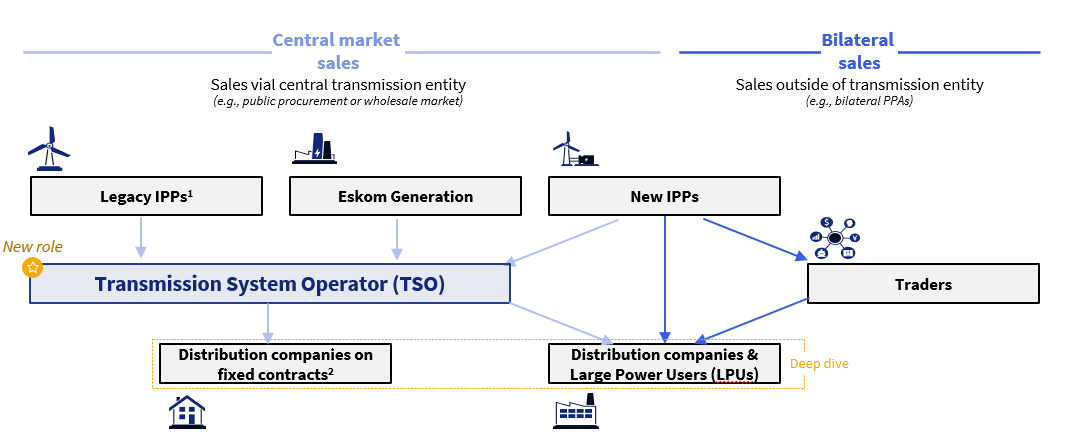

An independent Transmission System Operator (TSO) is a key enabler to a competitive multi-market. The TSO will have four functions:

In this new model, all legacy power purchase agreements (PPAs) and Eskom coal-fired generators will be placed on 5 year vesting contracts that effectively push generation capacity from coal into a competitive market – where some coal capacity will be “out of the money”.

South Africa needs an unprecedented generation and transmission infrastructure rollout to ensure its energy security and economic growth, and to #energisemzansi.

There are 3 main drivers for South Africa’s market reform:

The State and Eskom have limited funds.

They have high debt and a constrained balance sheet, and will not be able to fund the entire R1.8-trillion needed over the next 10 years.

There is also investment uncertainty. Developers will need to be sure that they will obtain a fair return on their investment if they’re to put such large amounts behind the expansion.

There is also a growing need for industrialisation and job growth. If we attract sufficient investment, we will be able to drive industrial investment, growth and sustainable job creation across several value chains, and #energisemzansi.

There are some risks that need to be managed during market reform such as a reduced security of supply. If the market is fully competitive, investments might move away from reliable energy sources and focus on cheaper options which could make energy supply less stable.

Price volatility is also a potential risk. In a competitive market, prices could fluctuate a lot. This means electricity could become unaffordable when there’s not enough supply.

Finally, there are South Africa’s broader development objectives. Without some degree of market control, it might be hard to meet certain development goals. For example, programmes to help poorer areas or specific targets for energy types might not happen on their own without intervention.

We need to ensure that market reform is implemented in a way that secures energy availability, affordability and sustainability.

Market reform is the most critical element of South Africa’s energy system. But to ensure market reform happens successfully, a lot more work needs to be done to #energisemzansi.

#EnergizeMzansi

We need market reform now

Physical Address:

12 Desmond Street,

Kramerville, 2148, South Africa

Enquiries:

Email: info@energycouncil.org.za

© 2025 Energy Council of South Africa.

All rights reserved | Privacy Policy | Fraud and Unethical Conduct

| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |

A Power Purchase Agreement (PPA) is a long-term contract between a buyer and a supplier of electricity that defines the terms of the agreement.

Multi-market system – a hybrid market model designed to accommodate various defined transactions (market transactions, physical bilateral transactions and regulated transactions).

Scheduling supply to meet current demand for electricity

Electricity storage encompasses all technologies that can consume electricity (e.g., charge in times of oversupply) and return it later (e.g., discharge in times of undersupply).

The capacity factor is the ratio of the actual electrical energy output over a certain period of time to the maximum possible output if the power source was operating at full capacity all the time. Essentially, it illustrates the efficiency and dependability of an energy source.

A transmission grid is an interconnected network of electrical transmission lines that moves electricity from power plants to distribution systems and end users

Variable renewable energy (VRE) or intermittent renewable energy sources (IRES) are renewable energy sources that are not adjustable due to their fluctuating nature, such as wind power and solar power

Capital costs are fixed, one-time expenses incurred on the purchase of equipment used in the production of goods

The cost added by producing one additional unit of a product or service.

Renewable energy refers to energy generated from a source that is not depleted when used

Liquefied natural gas (LNG) is natural gas that has been cooled down to liquid form for ease and safety of non-pressurized storage or transport.

Republic of Mozambique Pipeline Investments Company

A petajoule (PJ) is a unit of energy measurement that is equal to one million billion joules (10 to the power 15). It can also be expressed as 278 gigawatt hours. One petajoule is equal to 31.60 million cubic meters of natural gas.

Dispatchable generation refers to sources of electricity that can be programmed on demand at the request of power grid operators, according to market needs. Dispatchable generators may adjust their power output according to an order.

Domestic gas is natural gas found underground within a county’s borders

Energy Availability Factor (EAF) = measure of generation performance, electricity available to be generated. EAF is the difference between the maximum availability and all unavailabilities expressed as a percentage

Particulates are microscopic particles of solid or liquid matter suspended in the air. Sources of particulate matter can be natural or anthropogenic. They have impacts on climate and precipitation that adversely affect human health, in ways additional to direct inhalation.

Nitric oxide (NO) and nitrogen dioxide (NO2) are two gases whose molecules are made of nitrogen and oxygen atoms. These nitrogen oxides contribute to the problem of air pollution, playing roles in the formation of both smog and acid rain. They are released into Earth’s atmosphere by both natural and human-generated sources.

Sulfur oxides are a group of molecules made of sulfur and oxygen atoms, such as sulfur dioxide (SO2) and sulfur trioxide (SO3). Sulfur oxides are pollutants that contribute to the formation of acid rain, as well as particulate pollution. Some are released into Earth’s atmosphere by natural sources, but most are the result of human activities.

Net Zero means cutting carbon emissions to a small amount of residual emissions that can be absorbed and durably stored by nature and other carbon dioxide removal measures, leaving zero in the atmosphere.

Nationally Determined Contributions are the commitments that countries make to reduce their greenhouse gas emissions as part of climate change mitigation.

The Paris Agreement is a legally binding international treaty on climate change. It was adopted by 196 Parties at the UN Climate Change Conference (COP21) in Paris, France, on 12 December 2015.

The energy trilemma is a framework that energy policymakers use to balance three objectives:

likely to receive funding

The EU’s Carbon Border Adjustment Mechanism (CBAM) is the EU’s tool to put a fair price on the carbon emitted during the production of carbon intensive goods that are entering the EU, and to encourage cleaner industrial production in non-EU countries

An integrated system brings together several elements to create single cohesive unit

Green hydrogen is hydrogen produced by the electrolysis of water, using renewable electricity. Production of green hydrogen causes significantly lower greenhouse gas emissions than production of grey hydrogen, which is derived from fossil fuels without carbon capture.